If you think the lowest interest rate is the only metric that matters for your aviation career, you might be stalling your progress before you even clear the runway. It's completely natural to feel a bit of turbulence when looking at 2026 interest rates. With undergraduate Direct Loans at 6.52% and some private options reaching double digits, the fear of debt without a guaranteed job is a heavy weight to carry. You want to focus on your checkride, not how you'll manage high monthly payments while still building your hours.

We understand that the path to a $226,600 median pilot salary requires a smart financial flight plan. This guide helps you master the complexities of student loans vs personal loans for flight school so you can discover which structure accelerates your path to the flight deck. You'll learn how to leverage 2026 updates, like the Working Families Tax Cuts Act and expanded 529 plans, to secure deferred repayment options and lower costs. We will preview how these choices impact your journey through our Career Pilot Program or Airline Pilot Elite track, ensuring you reach seniority faster and maximize your long-term earning potential.

Key Takeaways

- Understand how 2026 regulatory shifts and historic pilot salaries change the math on your training investment.

- Evaluate the critical differences between fixed and variable rates to keep your monthly payments manageable during time-building.

- Discover when the flexibility of student loans vs personal loans for flight school makes the most sense for your specific training timeline.

- Learn how to leverage expanded 529 plans and merit-based lending to lower your barrier to entry.

- Identify how professional training tracks like the Airline Pilot Elite program help you demonstrate value to lenders and reach the flight deck sooner.

Navigating Flight Training Financing Options in 2026

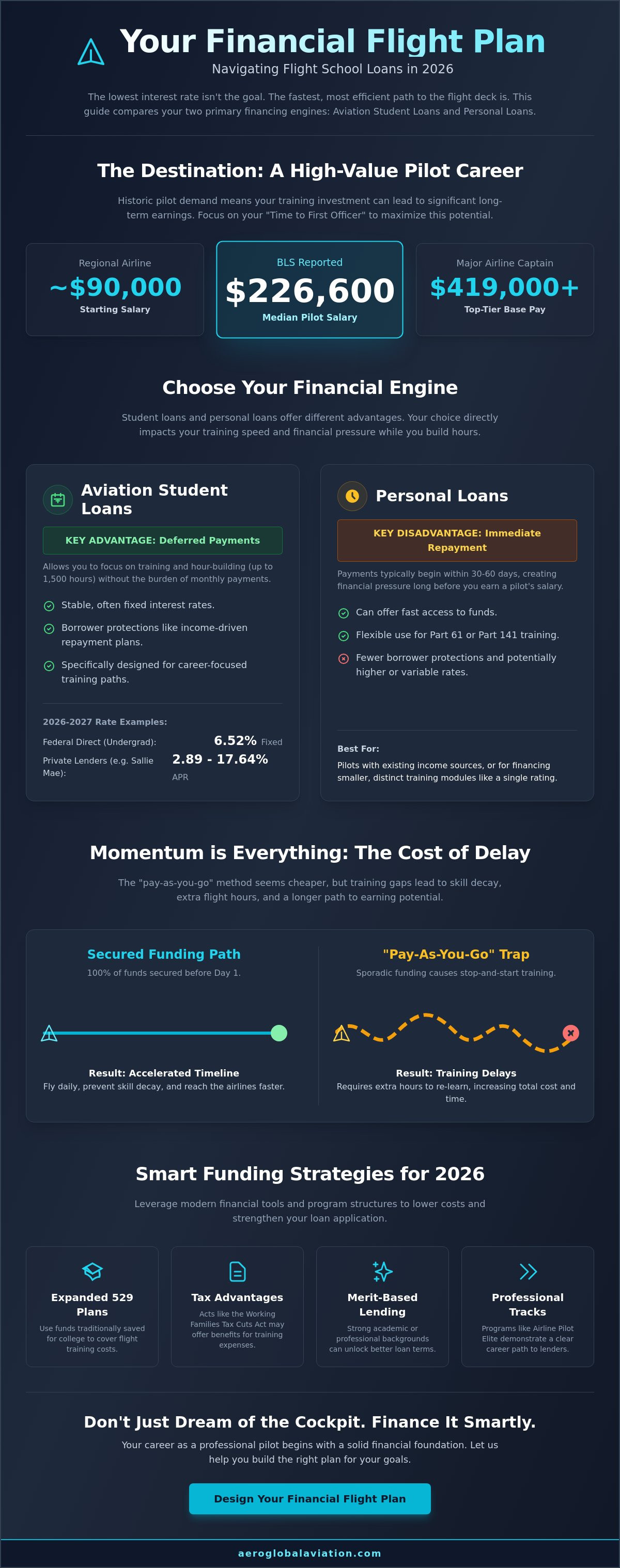

Securing capital for your flight training is the first real checkride of your career. In 2026, the aviation industry is witnessing historic highs in compensation, with major airline captains earning base pay between $288,000 and $419,000. This massive earning potential is driven by a persistent pilot shortage and mandatory retirements, creating roughly 18,200 openings each year according to the Bureau of Labor Statistics. Deciding between student loans vs personal loans for flight school is about more than just interest rates; it's about momentum. While a standard four-year degree relies heavily on the Federal Direct Student Loan Program, flight training requires a more aggressive, career-focused capital structure.

The primary metric for your success isn't just the total debt, but your "Time to First Officer." Every month you spend waiting for funds or training part-time is a month you aren't earning a regional airline salary, which currently starts around $90,000. You can use our Professional Pilot Track as a benchmark for what a full-scale career investment looks like. Financing this path requires a strategy that mirrors the high-stakes nature of the cockpit, prioritizing speed and training continuity over traditional academic cycles.

The Cost of Becoming a Professional Pilot

There's a significant difference between earning a private certificate and preparing for the airlines. A course like our Wings Foundation focuses solely on the PPL, whereas the Career Pilot Program covers the full journey to a commercial certificate. Many students fall into the "pay-as-you-go" trap, thinking it saves money. In reality, training gaps lead to skill decay, requiring extra flight hours to relearn maneuvers you've already practiced. Beyond tuition, you must account for "hidden" costs like FAA checkride fees, navigation gear, and living expenses during full-time training. Comparing student loans vs personal loans for flight school requires you to think like a captain, prioritizing reliability over the lowest possible initial cost.

Why Your Choice of Loan Impacts Your Training Speed

Consistency is the secret to finishing your ratings on schedule. When you have 100% of your funds secured before Day 1, you can fly daily and take advantage of our regional climate's excellent flying weather. This accelerated timeline prevents the mental fatigue that comes with stop-and-start training. As your practical mentor, we recommend having a clear budget that covers your entire syllabus through the Airline Pilot Elite program. Secured funding ensures that when the weather is clear and an instructor is ready, you're in the air, not waiting for a bank transfer to clear. This proactive approach turns your professional goals into a tangible destination.

Deep Dive into Aviation Student Loans: Federal and Private Routes

Choosing the right path for your aviation capital requires understanding that not all debt is created equal. In 2026, your eligibility for specific funding depends heavily on whether you choose Part 61 vs. Part 141 training. While federal student aid is often tied to university-affiliated programs, private lenders provide the flexibility needed for accelerated flight academies. When weighing student loans vs personal loans for flight school, you'll find that specialized aviation student loans offer features that personal loans lack, specifically the ability to defer payments while you build the 1,500 hours required for your ATP certificate.

Interest rates in the 2026 market vary significantly. For the 2026-2027 academic year, federal undergraduate Direct Loans are set at a fixed 6.52%, while Direct PLUS Loans for parents sit at 9.07%. Private lenders offer a wider range; for instance, Sallie Mae fixed rates can span from 2.89% to 17.64% APR depending on creditworthiness. The key is to find a structure that doesn't drain your bank account while you're still in the cockpit earning your ratings. Deferred repayment is your best friend during the time-building phase, allowing you to focus on your skills rather than a monthly bill.

Federal Student Loans: Pros and Cons

To access federal funds, you must complete the FAFSA. These Title IV loans offer stable interest rates and vital protections like income-driven repayment plans, which are incredibly helpful during your first year as a flight instructor. However, the Working Families Tax Cuts Act of 2025 has introduced new loan limits for 2026, and the phasing out of the Graduate PLUS Program means many students face a "funding gap." Federal caps often don't cover the full cost of advanced training, forcing students to look elsewhere for the remaining balance.

Private Aviation Loans: The Specialized Alternative

Specialized lenders like Stratus Financial or Sallie Mae "speak aviation" and understand the high ROI of a pilot career. They often provide some of the Best Flight School Loans by using merit-based lending models. These lenders look at your future earning potential and past academic success rather than just a credit score. Having a co-signer is still a powerful tool to secure the most competitive 2026 rates. If you want to see how these financial tools apply to a professional curriculum, you might explore our Career Pilot Program to see how our syllabus aligns with lender requirements.

Whether you choose federal or private routes, the goal remains the same: secure 100% of your funding before you start. This ensures your training remains continuous and your focus stays on the horizon. By mastering the nuances of student loans vs personal loans for flight school, you position yourself to enter the airline industry with a manageable financial profile and a clear path to the captain's seat.

The Role of Personal Loans in Fast-Track Flight Training

While specialized student debt is the standard for long-term career tracks, personal loans serve as a high-speed alternative for specific training milestones. They offer a level of flexibility that traditional educational products can't match because they lack "academic oversight." When you use a personal loan, the lender doesn't monitor your enrollment status or syllabus progress; they simply provide the capital based on your creditworthiness. This makes them a strategic choice for pilots who need to move quickly, especially when comparing student loans vs personal loans for flight school for modular training or filling small funding gaps.

The biggest advantage here is the speed of funding. In the competitive 2026 aviation market, getting into the cockpit in Kissimmee even a few weeks earlier can mean reaching your seniority number faster. Personal loans often land in your bank account within days, allowing you to take advantage of the excellent Florida flying weather without waiting for school-certified disbursements. If you're looking to complete a focused course like our Wings Foundation to secure your PPL, this immediate access to capital keeps your momentum high.

Flexibility and Speed: The Personal Loan Advantage

Major personal lenders in 2026 have streamlined their application-to-funding timelines, often completing the process in 24 to 72 hours. This is significantly faster than the weeks required for federal or private student loan certifications. These loans are excellent for covering "the gap" in commercial pilot training costs that federal caps might not reach. You can also look into specialized options like the AOPA Flight Training Finance program, where rates in May 2026 range from 11.74% to 13.74% APR. Using a personal line of credit for a modular PPL-only course ensures you aren't over-borrowing for ratings you haven't started yet.

Risks to Consider: Repayment and Interest

You must be aware of the "immediate repayment trap." Unlike the deferred student loans we discussed earlier, personal loans typically require you to start paying back the principal and interest the very next month. This can be difficult if you're training full-time and don't have a steady income yet. Personal loans also lack the robust forbearance or deferment options found in educational lending, meaning there's less of a safety net if your training is delayed. In 2026, lenders generally require your total monthly debt obligations to remain within a specific percentage of your gross income to qualify for the most competitive rates. When evaluating student loans vs personal loans for flight school, remember that the speed of a personal loan comes at the cost of more rigid repayment terms.

Student Loans vs. Personal Loans: A Strategic Comparison for Pilots

Choosing between student loans vs personal loans for flight school isn't just a financial decision; it's a strategic move that dictates how quickly you reach the flight deck. A student loan is structured like a heavy-lift transport, designed to carry the full weight of a professional career track with built-in safeguards. A personal loan is more like a light utility aircraft, offering speed and agility for specific, short-term needs. To help you decide which vehicle fits your mission, we've broken down the core mechanics of each option below.

| Feature | Specialized Student Loan | Personal Loan |

|---|---|---|

| Interest Rates | Fixed or Variable (often lower) | Typically Fixed (can be higher) |

| Repayment | Deferred until after training | Immediate (starts next month) |

| Eligibility | Requires school certification | Credit-based; no school oversight |

The biggest hurdle for most students is the fear of monthly payments while building the 1,500 hours required for an ATP certificate. During this time, you'll likely work as a Certified Flight Instructor (CFI). While the median pilot wage is high, a CFI's starting income is more modest. Specialized student loans solve this by allowing for interest-only payments or full deferment during your time-building phase. This protects your credit score during your first airline job, ensuring you don't enter the industry with a tarnished financial record. Once you've selected your funding, you can evaluate the Best Flight Schools in Florida to ensure your capital is being invested in high-quality equipment and instruction.

The Repayment Timeline: CFI Phase vs. Airline Phase

Your financial journey has two distinct stages. In the CFI phase, your goal is survival and hour-building. Using "interest-only" payment options during this period is a life-saver, keeping your monthly obligations low while you gain experience. Once you transition to a Regional First Officer role, where starting salaries in 2026 hover around $90,000, you can begin aggressive repayment. A significant 2026 trend is the use of airline sign-on bonuses to make large balloon payments on the principal, effectively "clearing the runway" of debt much faster than traditional schedules allow.

Choosing Based on Your Career Goal

If you're a career-focused pilot, a specialized student loan is almost always the superior choice because it aligns with the long-term ROI of the industry. For hobbyists or modular students finishing a single rating, the speed of a personal loan might be worth the higher interest. Remember that pilot training in Kissimmee offers a unique advantage: the favorable climate allows for more flight days per year. This means you finish faster, start earning sooner, and hit your "break-even" point much earlier. You should calculate this point using 2026 salary data to see exactly when your increased earnings will outpace your loan costs. Ready to start your journey? Explore our Airline Pilot Elite program to see how we fast-track your path to the airlines.

Financing Your Career at Aero Global Aviation Academy

At Aero Global Aviation Academy, we don't just teach you how to fly; we help you build the financial flight plan required to reach your professional goals. We recognize that the choice between student loans vs personal loans for flight school can feel overwhelming when you're also trying to master aerodynamics and navigation. Our role as your practical mentor is to provide the clarity you need to make an informed investment in your future. By training in the Kissimmee and Orlando region, you benefit from a unique regional advantage. Our local climate provides a high number of flyable days each year, which directly translates to financial efficiency. Fewer weather delays mean you complete your ratings on schedule, which helps you avoid the extra interest costs associated with extended training timelines.

Our structured approach is designed to get you into a paying cockpit as quickly as possible. When you finish your training faster, you start earning that airline salary sooner, which is the ultimate way to offset your initial investment. We focus on transparency and realistic budgeting, ensuring you have a clear view of your path from the first day of ground school to the day you earn your commercial certificate. This commitment to your success is why we are a dedicated local partner for so many aspiring pilots in the 2026 market.

Our Partner Lenders and Financial Mentorship

Our career advisors take a hands-on approach to your financial success by reviewing your budget and helping you understand the requirements of various lenders. Because we are a professional academy that lenders trust, our students often find the application process more straightforward. The Airline Pilot Elite program is a preferred track for many financial institutions because it follows a comprehensive, predictable syllabus from a private pilot license to advanced instructor certifications. This structured curriculum reduces lender risk because it shows a clear, professional progression toward a high-paying career. We help you evaluate student loans vs personal loans for flight school to ensure your capital structure matches your specific career milestones.

Take the Next Step Toward the Flight Deck

Your journey to the airlines starts with a single decision. We encourage you to book a discovery flight at our Kissimmee facility to experience our training environment firsthand and validate the investment in your future. We also invite you to join our "Financing the Cockpit" sessions, where our mentors discuss 2026 lending trends and repayment strategies in a collaborative, supportive setting. Whether you are looking at the foundational Wings Foundation course or the full Career Pilot Program, we are here to help you secure the funding you need. Explore our Career Pilot Program and Financing Options today and let's turn your aviation aspirations into a professional destination.

Secure Your Future in the Sky

Your path to the flight deck is closer than you think. By understanding the strategic differences between student loans vs personal loans for flight school, you've already cleared the most difficult hurdle in your professional journey. Your choice must align with your specific destination. Specialized student loans offer the deferment you need for full-time career tracks; however, personal loans provide the rapid capital required for modular milestones. Both are tools designed to get you into the cockpit, provided you have a clear plan for your training and repayment.

Choosing the right academy is just as critical as choosing the right loan. Our accelerated 2026 Career Pilot Track is designed to maximize every dollar by leveraging Kissimmee’s 300 plus flying days per year. This efficiency, combined with our deep partnerships with leading aviation lenders, ensures you spend less time in training and more time earning a seniority number. Don't let financing complexities ground your dreams. Take control of your career path today by reviewing your options with mentors who understand your goals.

Launch your career with Aero Global Aviation Academy—View our Financing Guide

We are ready to welcome you to the cockpit and support you every step of the way toward your professional wings.

Frequently Asked Questions

Can I get a student loan for flight school if it is not part of a degree program?

Yes, private student loans are specifically designed for non-degree flight training at professional academies. While federal loans often require university affiliation, private lenders partner with academies to fund career-focused tracks like our Career Pilot Program. This is a primary reason students compare student loans vs personal loans for flight school, as specialized student loans offer educational protections that general personal loans do not.

What is the average interest rate for flight school loans in 2026?

Rates for 2026 vary by lender and your specific credit profile. Federal undergraduate loans are fixed at 6.52% for the 2026-2027 academic year, while private aviation lenders offer fixed rates ranging from 2.89% to 17.64% APR. If you have excellent credit (720 or higher), personal loan options average around 13.76% fixed, though specialized aviation products often provide more competitive terms for dedicated students.

Do flight school loans cover living expenses and housing in Orlando?

Many private student loans allow you to borrow enough to cover both tuition and cost-of-living expenses. This ensures you can focus entirely on your training at our Kissimmee facility without the distraction of a full-time job. You should verify the specific cost of attendance caps with your lender, as they often include housing, materials, and FAA checkride fees in the approved loan amount.

Is it better to pay for a Private Pilot License (PPL) with cash or a loan?

Paying cash for your PPL through a course like our Wings Foundation is often the most cost-effective route if you have the savings available. It avoids interest accumulation and keeps your credit clear for larger career-focused financing later. However, if using a loan allows you to train full-time and finish faster, the speed advantage can outweigh the interest costs by getting you to a professional salary sooner.

What credit score is needed for a flight school loan without a co-signer?

Most lenders look for a credit score of 720 or higher to approve a flight school loan without a co-signer. Borrowers with scores below this threshold often face higher interest rates or may be denied altogether. Using a co-signer with strong credit is a common strategy to secure the most favorable 2026 rates and lower your overall debt burden while you are in the training phase.

Are there any flight school loans with deferred payments until I reach the airlines?

Yes, specialized aviation student loans often offer deferred repayment or interest-only options while you are in training and building your 1,500 hours. This is a major factor when weighing student loans vs personal loans for flight school, as personal loans usually require immediate repayment. These deferment periods protect your cash flow while you are working as a flight instructor or building time toward your ATP certificate.

Can I use a 529 plan to pay for flight training at Aero Global Aviation Academy?

As of 2026, federal changes like the "One Big Beautiful Bill Act" allow 529 plan funds to be used for FAA-certified vocational flight training. You can use these tax-advantaged funds to pay for tuition or even to pay down up to $10,000 of qualified student loans. We recommend consulting with a tax professional to ensure your specific plan distributions meet the current 2026 guidelines for vocational training expenditures.

What happens if I lose my medical certificate while I still have flight school debt?

Losing your medical certificate does not automatically cancel your loan obligations, but some specialized aviation lenders offer "loss of medical" insurance options. It is a smart move to look into private insurance policies that can cover your loan payments if a health issue grounds you. Always review the fine print of your loan agreement to understand the specific protections available for career-ending medical events.